Role

Product Designer

Client

Senior Capital

Duration

4 months

Time reading

5 minutes

Senior Capital App - Learn & Invest

PROBLEM

What's currently happening?

The population aged 60+ is rapidly growing and many older adults are being left behind by the increasing digitalization of financial services. Most existing banking and investment apps are designed for digitally fluent users, resulting in complex interfaces that fail to accommodate cognitive, visual, and motor limitations. As a result, older adults often struggle to confidently manage their finances, leading to: - High friction when using digital banking tools. - Increased dependence on others. - Greater vulnerability to fraud and poor financial decisions. This creates not only a usability problem, but also a product opportunity.

INSIGHTS

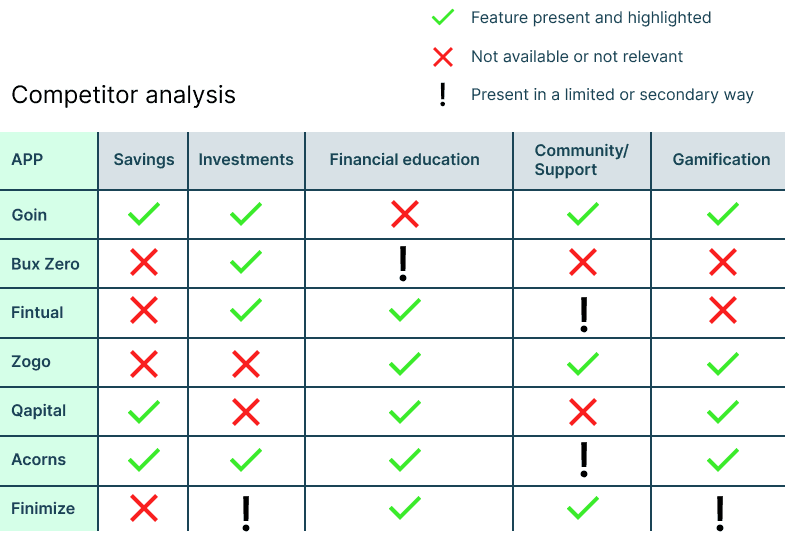

Market insights (Benchmarking)

I analyzed several investment and financial education apps such as Goin, Bux Zero and Fintual. While some platforms offer simplified interfaces and gamified experiences, most are clearly designed for younger, digitally fluent users. Key gaps identified: - Limited educational support for beginners. - Interfaces that still require high digital literacy. - Visual language and tone not aligned with older users. OPPORTUNITY: A product that prioritizes clarity, guidance and trust over speed and complexity.

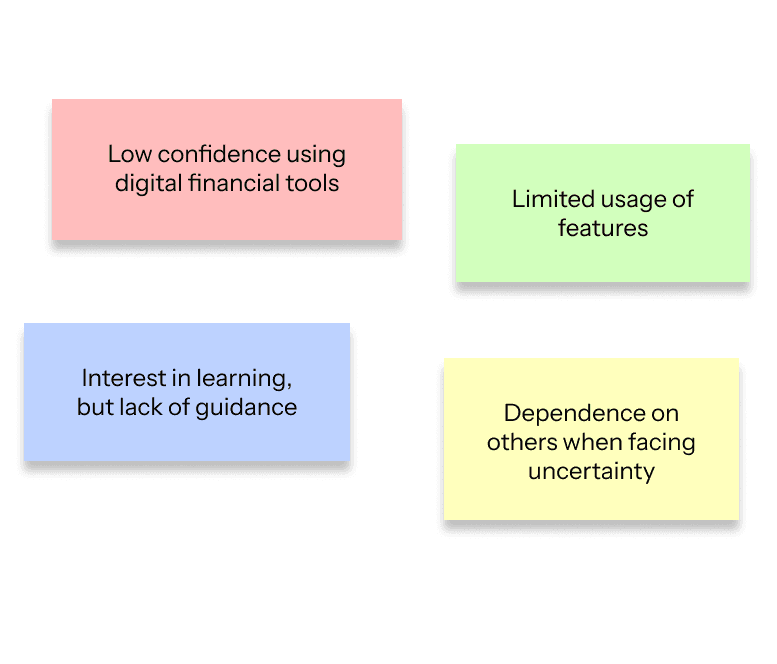

User insights (Interviews)

I conducted 5 semi-structured interviews with older adults to explore their needs, barriers, and motivations. This is what they said:

1. “I’d like the app to be easy to use. The thing is, they’re usually not, at least not for people like me.” 2. “I only use basic things.” 3. “I’d like to learn more about how to grow my savings or invest my money.” 4. “If there’s something I don’t understand, I ask to a family member.”

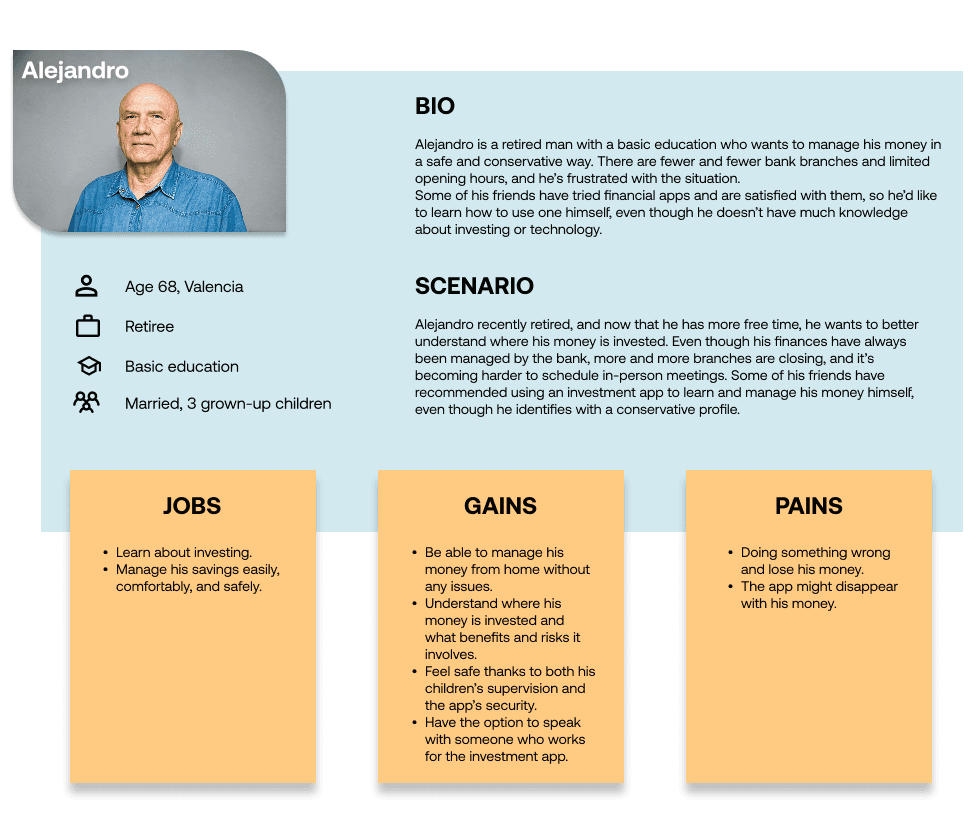

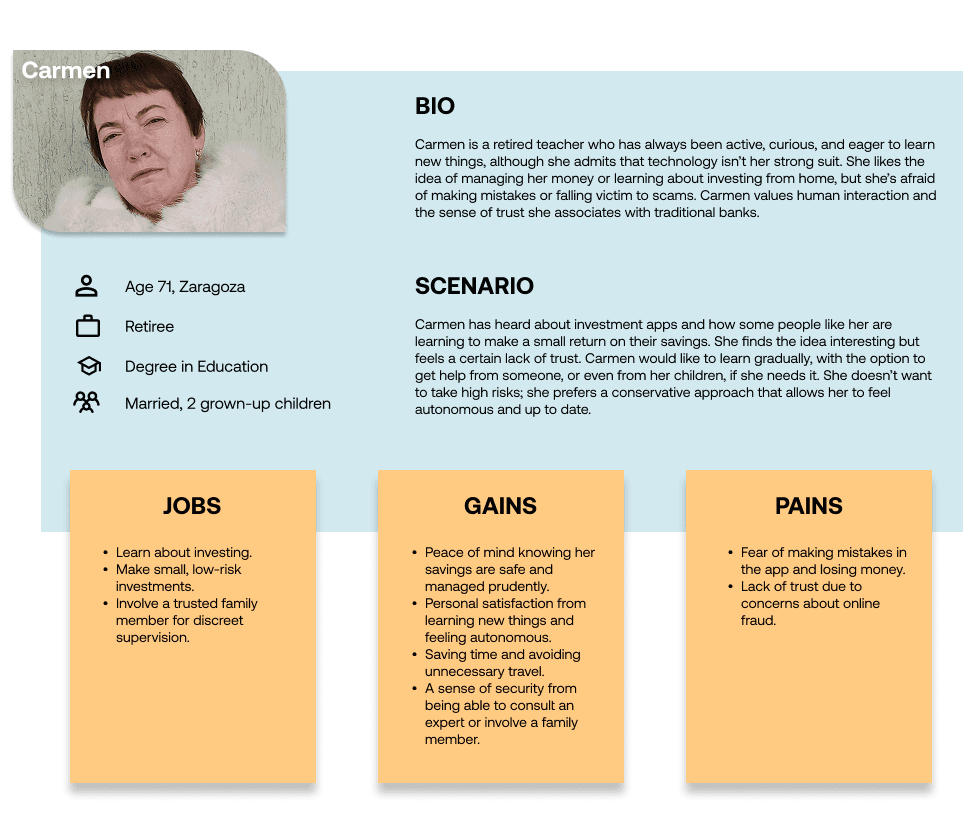

Personas

To align design decisions with user needs, I synthesized the research into key behavioral archetypes.

SOLUTION & DECISIONS

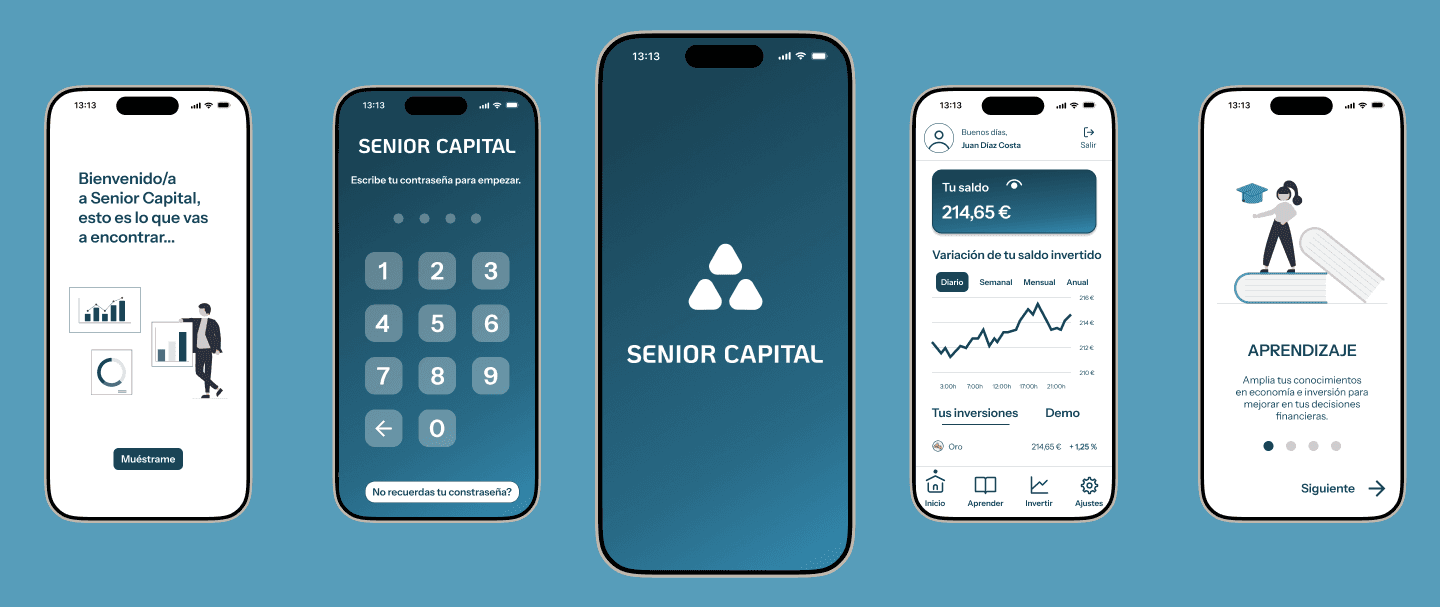

Senior Capital App

Based on the research insights, I designed a financial learning and investing experience tailored to older adults, focusing on confidence, simplicity, and guided decision-making. Rather than building a feature-rich product, I prioritized reducing cognitive load and supporting users step by step.

Key features

IMPACT & LEARNINGS

Reflection and takeaways

Although this project was not launched, I defined key success metrics to evaluate its effectiveness: - Reducing task completion time by 26% after user testing. - Improvement in user confidence when making financial decisions. - Growth in feature adoption beyond basic actions. The goal is to empower older adults to transition from passive users to confident decision-makers. Through this project, I learned that designing for this audience is less about adding features and more about reducing complexity and building trust.

Next steps

- Validate with real users over time: Run a mid-term usability and behavior test (3–6 months) to measure financial knowledge retention, changes in user behavior and trust and confidence levels. - Explore conversational support: Introduce a voice or chat assistant to reduce friction in complex tasks and provide real-time explanations in simple language. This could significantly improve accessibility for users with visual or motor limitations. - Strengthen the trust ecosystem: Evolve the Family Supervision feature into a lightweight financial wellbeing system, focused on detecting unusual activity and providing reassurance without compromising autonomy.